A tenant screening report is one of the most powerful tools landlords have to assess risk and find reliable tenants. But the report can be detailed and complex — unless you know what to look for.

What’s Included in a Landlord Studio Tenant Screening Report?

Here’s what’s covered in a typical report:

Personal details

Credit score (ResidentScore)

Tradelines (open credit accounts)

Collections

Credit inquiries

Public records (bankruptcies, civil judgments, tax liens)

Eviction records

Criminal records

AKAs (Also Known As)

Let’s break each one down below.

Personal Details

This section is provided by the applicant and includes:

Full name

Date of birth

Current and previous addresses

Note: Social Security Numbers are collected by TransUnion but are not shared with landlords to protect both parties and reduce liability.

Why it matters: Check the tenant’s personal details against their other records and ensure everything matches up. Discrepancies here could be a sign of fraud.

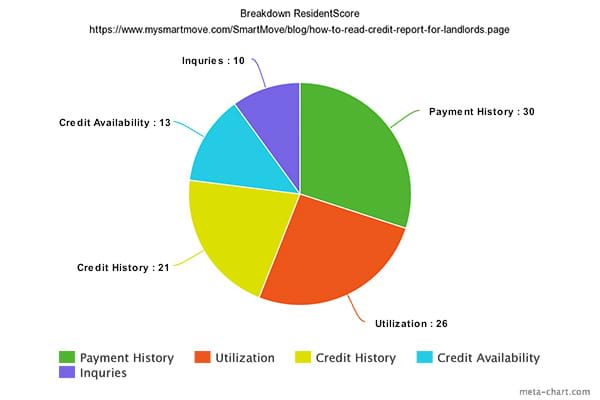

Credit Score (ResidentScore)

Landlord Studio reports show TransUnion’s ResidentScore. This is a renter-optimized credit score that’s between 300 and 850.

700+ = Excellent

650–699 = Good

600–649 = Fair

Below 600 = Potential risk

Why it matters: This gives you a quick insight into a tenant’s financial responsibility. The higher the score the more likely they are to have experience handling debt.

Remember that a credit score only tells part of the picture. For example, younger renters might have a low score because of a lack of credit history rather than a bad credit history, so always look at the full report, not just the score.

The ResidentScore weighs payment history more heavily than standard credit scores, making it more relevant for rental decisions.

Generally, landlords look for a minimum credit score of 600-650.

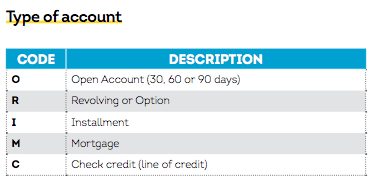

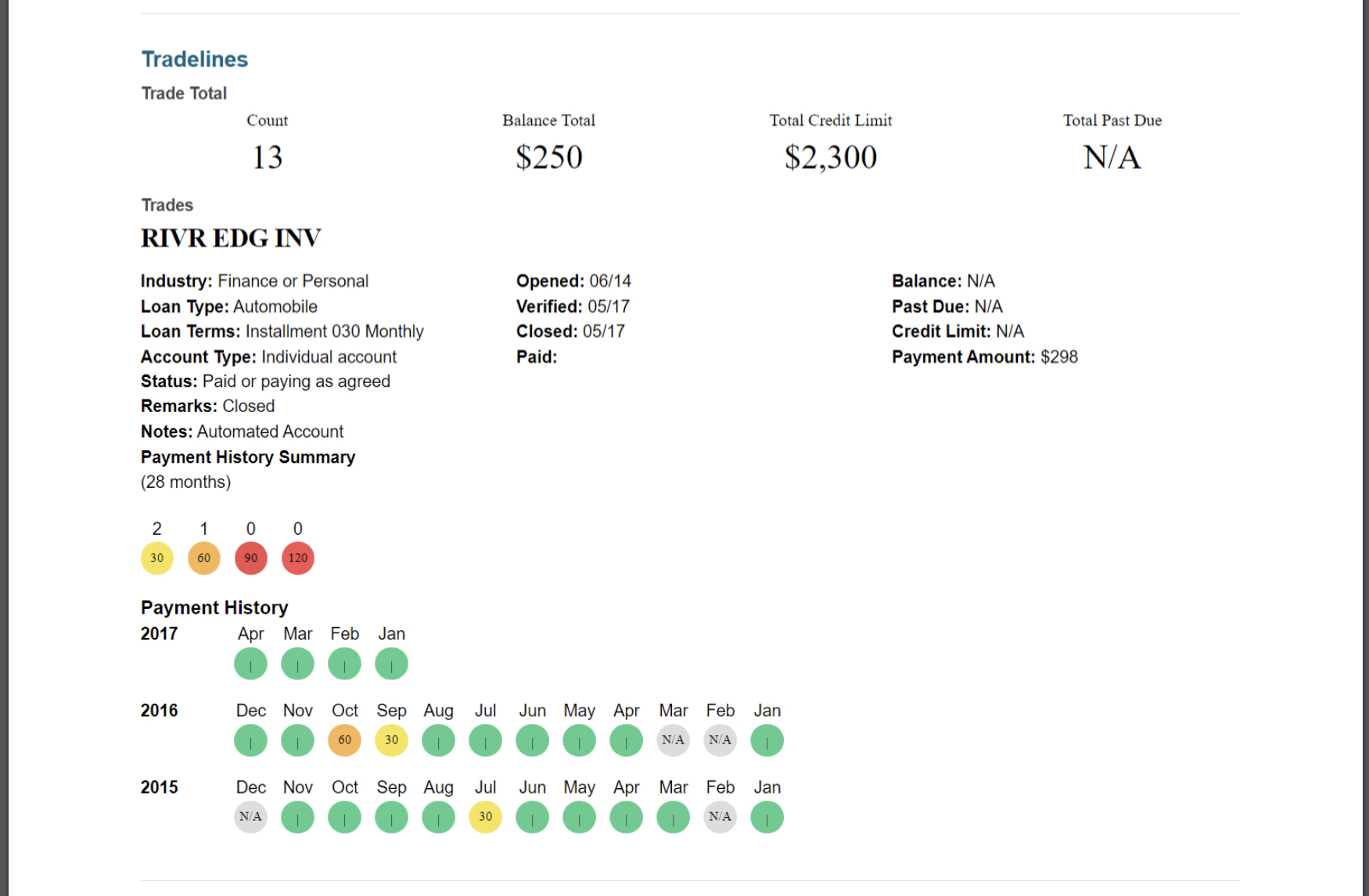

Tradelines

Tradelines are open credit accounts, including:

Credit cards

Student loans

Auto loans

Mortgages

Why it matters: Look for patterns like consistent on-time payments, which indicate reliability. But be cautious of high credit utilization, numerous open tradelines, and any history of missed payments, as these can be signs of financial mismanagement or stress.

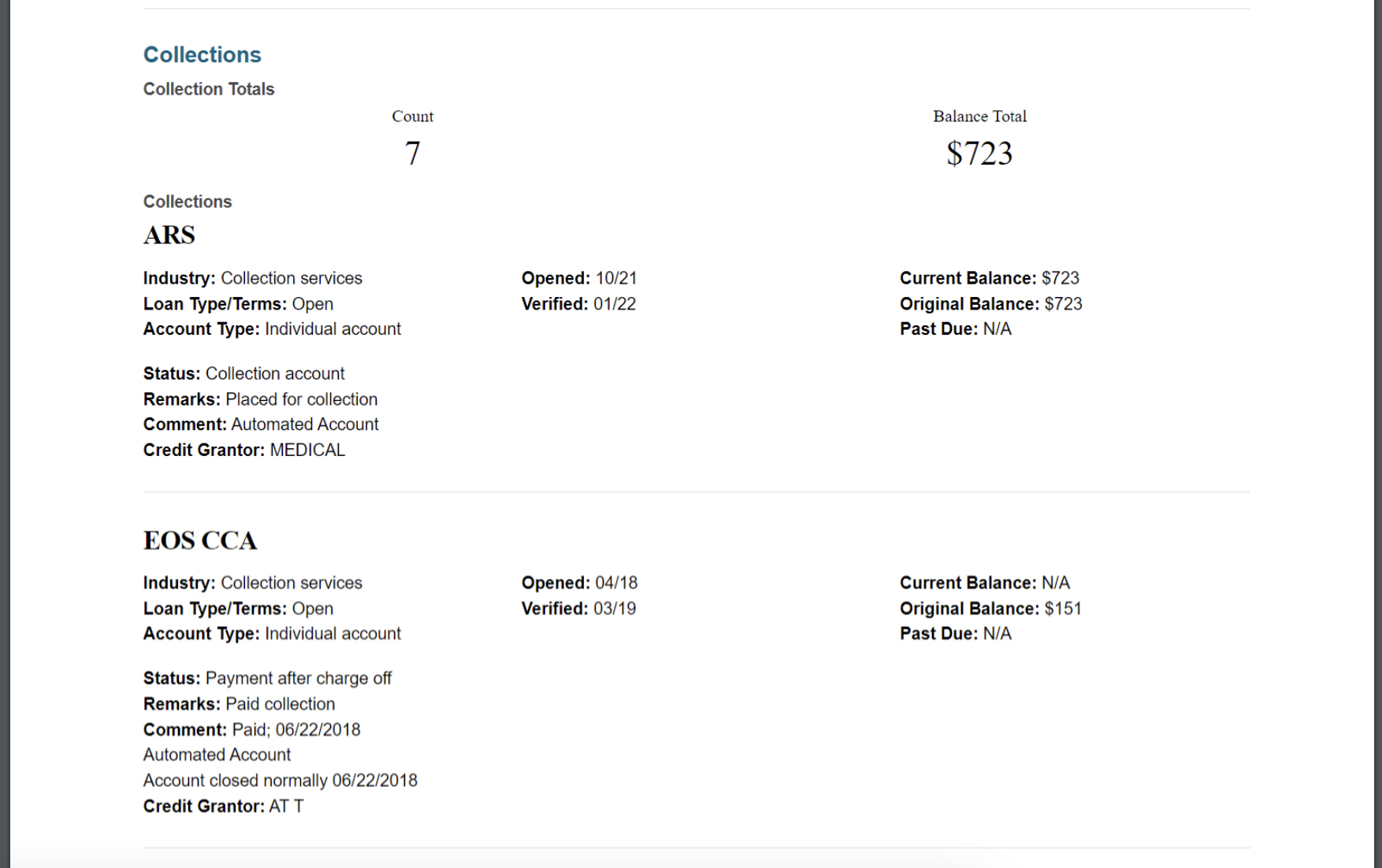

Collections

If an applicant fails to pay an account, it may be sent to collections (typically after 180 days).

Common collection accounts include:

Utilities

Credit cards

Medical bills

Cell phones

Why it matters: Watch out for accounts in collections, as these suggest the applicant has struggled to meet financial obligations in the past, which could indicate an inability to meet payments in the future.,

On top of this, accounts in collections mean they now have additional debts that they will be paying, which can directly impact their cash flow and ultimately their ability to pay rent.

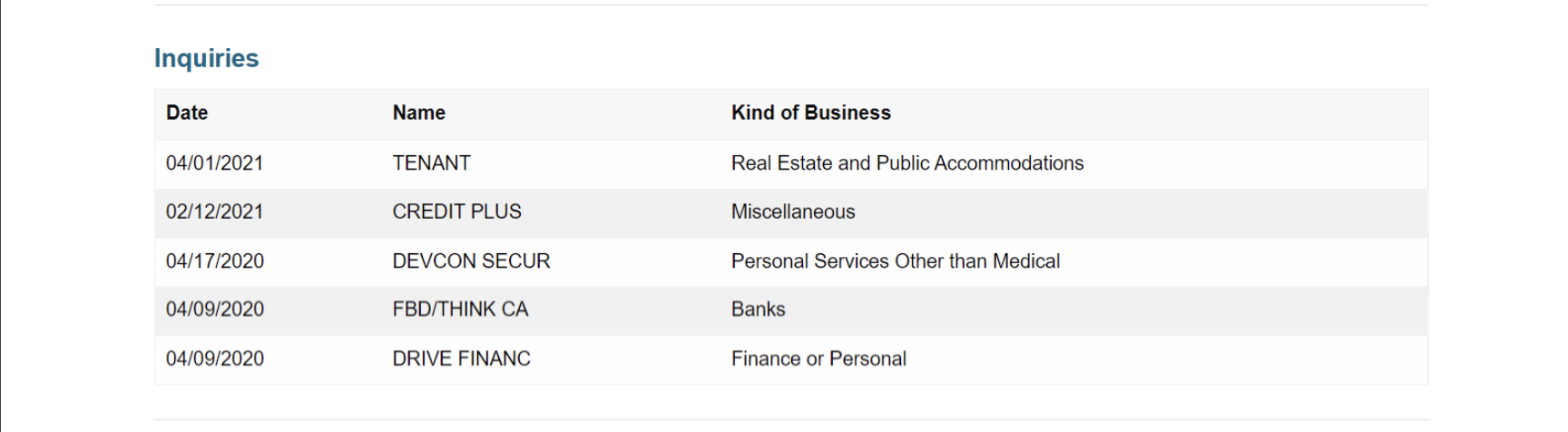

Inquiries

Inquiries are recent checks that have been carried out against the applicant's credit. Generally, these indicate that the tenant has applied for loans or credit cards.

Why it matters: Multiple recent hard inquiries (e.g., from loan or credit card applications) can suggest they’ve been attempting to get loans (either they’re taking out multiple loans, or they keep getting rejected). This could suggest financial instability or overextension.

Public Records

The public records shown on the Landlord Studio tenant screening report include:

Bankruptcies (Chapter 7 or Chapter 13)

Civil judgments (e.g., unpaid debts via court)

& Tax liens

Note that Chapter 7 bankruptcies (no repayment) stay on a report for 10 years, while Chapter 13 (partial repayment) stays on the report for 7. Many landlords reject Chapter 7 filings but may accept Chapter 13 with higher deposits.

Why it matters: Public records highlight serious financial issues like bankruptcies, judgments, or tax liens that may affect a tenant’s ability to pay rent. This information gives landlords context beyond a credit score, helping them assess risk, decide whether to require a higher deposit or co-signer, and ultimately protect rental income from potential defaults or evictions.

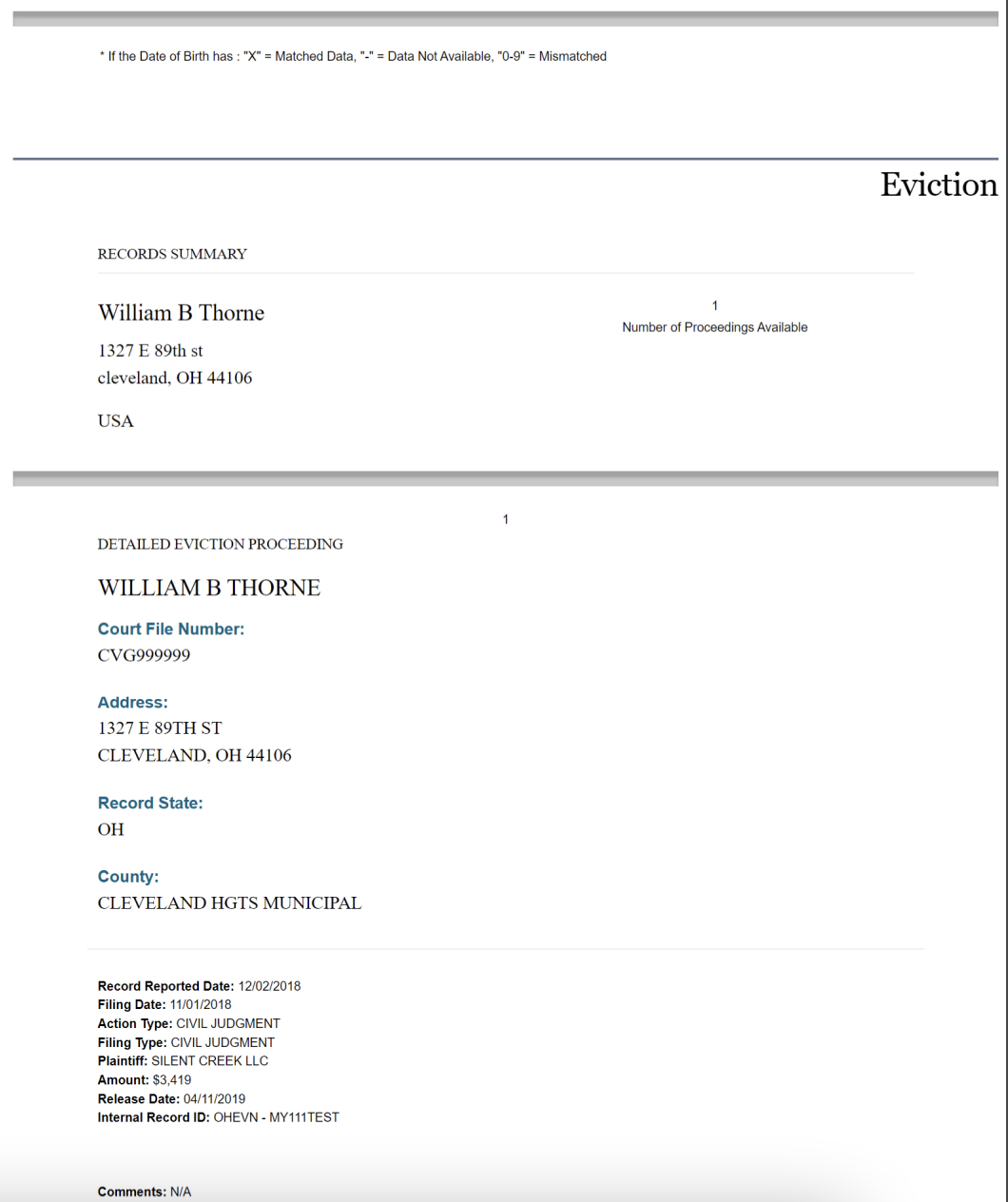

Eviction Records

A tenant's previous rental and eviction history is statistically one of the strongest predictors of future behavior, as it often reflects payment stress that can recur.

Eviction records include:

State and county

Case type (e.g. Forcible Entry/Detainer)

Plaintiff (landlord/property manager)

Judgment amount

Action date

Property address

Why it matters: There are numerous reasons a tenant might be evicted, and some of these factors are simply out of their control. Most often, though, evictions are initiated because of missed payments. So, while a previous eviction might not be an immediate disqualifier, tenants with a past eviction are statistically more likely to be evicted again, and you should definitely find out more about the eviction circumstances before proceeding.

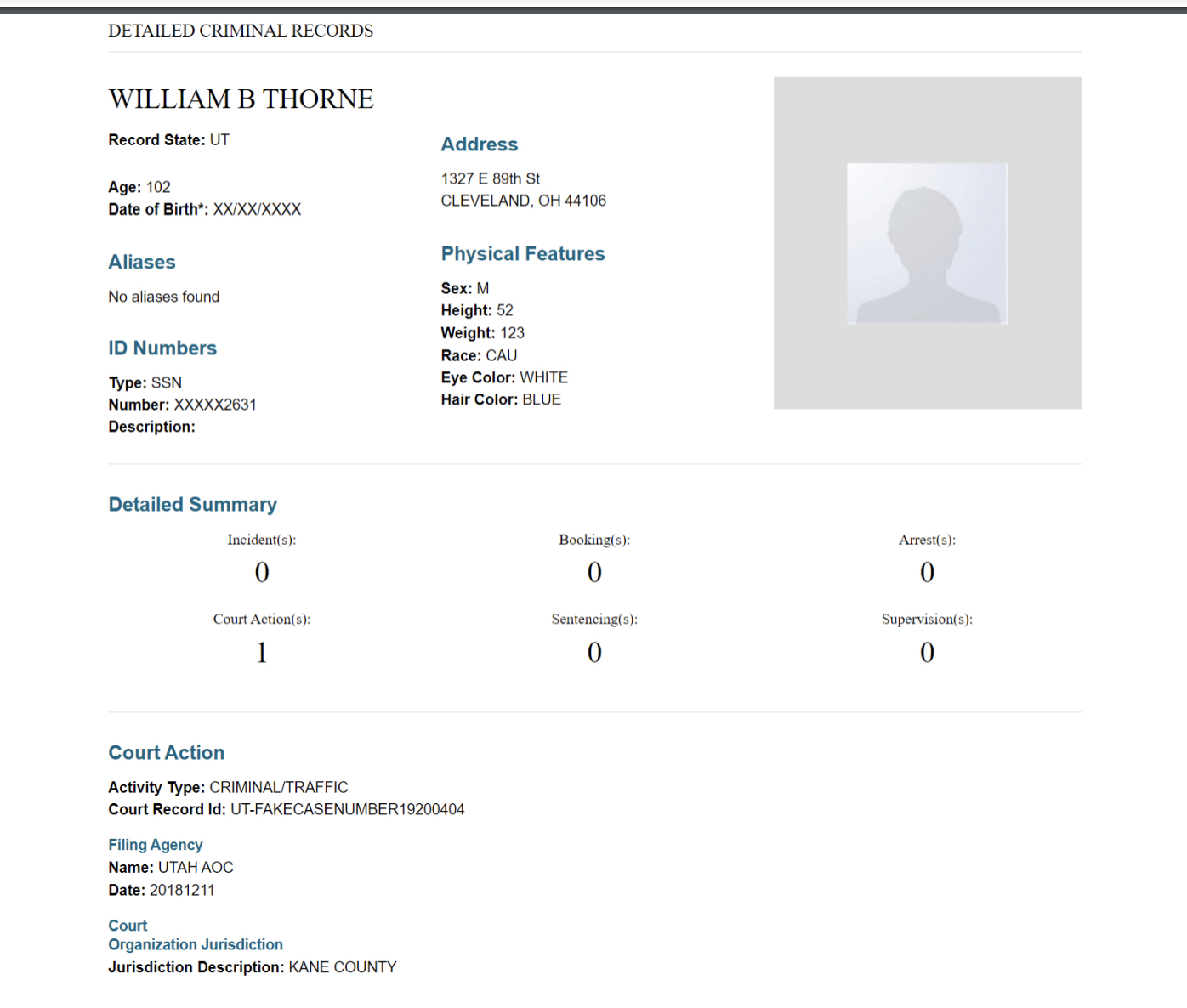

Criminal Records

SmartMove checks over 200 million state and federal records. But coverage varies by state/county.

Legal note: According to HUD and the FCRA, you cannot deny an applicant based solely on an arrest; the individual needs to have been convicted for this to be a contributing factor to your decision. Additionally, a conviction you use to make your decision must relate directly to a risk to your property (e.g., a conviction of financial fraud, violent behavior in multi-unit housing, or drug dealing).

Why it matters: Criminal records provide insight into potential risks to your property, other tenants, and the community. While not every record is grounds for denial, convictions related to violence, drug activity, or financial fraud may signal higher risk. Reviewing this information (while staying compliant with HUD, FCRA, and local laws) helps landlords make fair, informed decisions and maintain a safe rental environment.

This section lists any name variations that the applicant might be known as. For example:

Nicknames (e.g. “Mike” vs. “Michael”)

Maiden names

Legal name changes

Why it matters: Aliases ensure the background check is accurate and complete. Without checking all known name variations, important records (such as past evictions, criminal convictions, or credit issues) might be missed. Reviewing AKAs helps landlords confirm identity and avoid overlooking potential risks hidden under a different name.

What’s Not Included

Due to privacy and accuracy concerns, SmartMove does not include:

Employment verification — This can be verified through a manual check of an employer reference and/or signed employment agreement.

Proof of income documentation — Acceptable forms of proof of income include pay stubs, a copy of the signed employment agreement, or bank statements showing recent payments.

Social Security Numbers — Though the SSN is collected as part of the ID verification process, it is not shared with the landlord.

Landlord references — Landlords should manually check any landlord references that are provided as part of the rental application process.

Note: Applicants may self-report income, but it is not verified or included in the report output. You should ask for proof of income separately as part of the application process.

Final Tips for Using the Report

Set screening criteria in advance (e.g. minimum score, no recent evictions)

Stay consistent — apply your criteria equally to all applicants

Understand local screening laws — especially regarding criminal records

Keep documentation in case of disputes or fair housing claims

Start Screening with Confidence

With Landlord Studio, running and reviewing a tenant screening report is easy, fast, and secure.

Create a free account to start screening your next tenant with confidence.

.png)

.png)