If you accidentally became a landlord, inherited a property, or started renting out a former home, there is a good chance your rental finances still run through the same bank account you use for groceries, holidays, and household bills.

You are not alone. With more than 71.6% of U.S. rental properties owned by private individuals rather than companies or LLCs, many DIY and first-time landlords begin this way because it feels easier in the beginning. When there is only one property and a handful of expenses, mixing everything together may not seem like a problem.

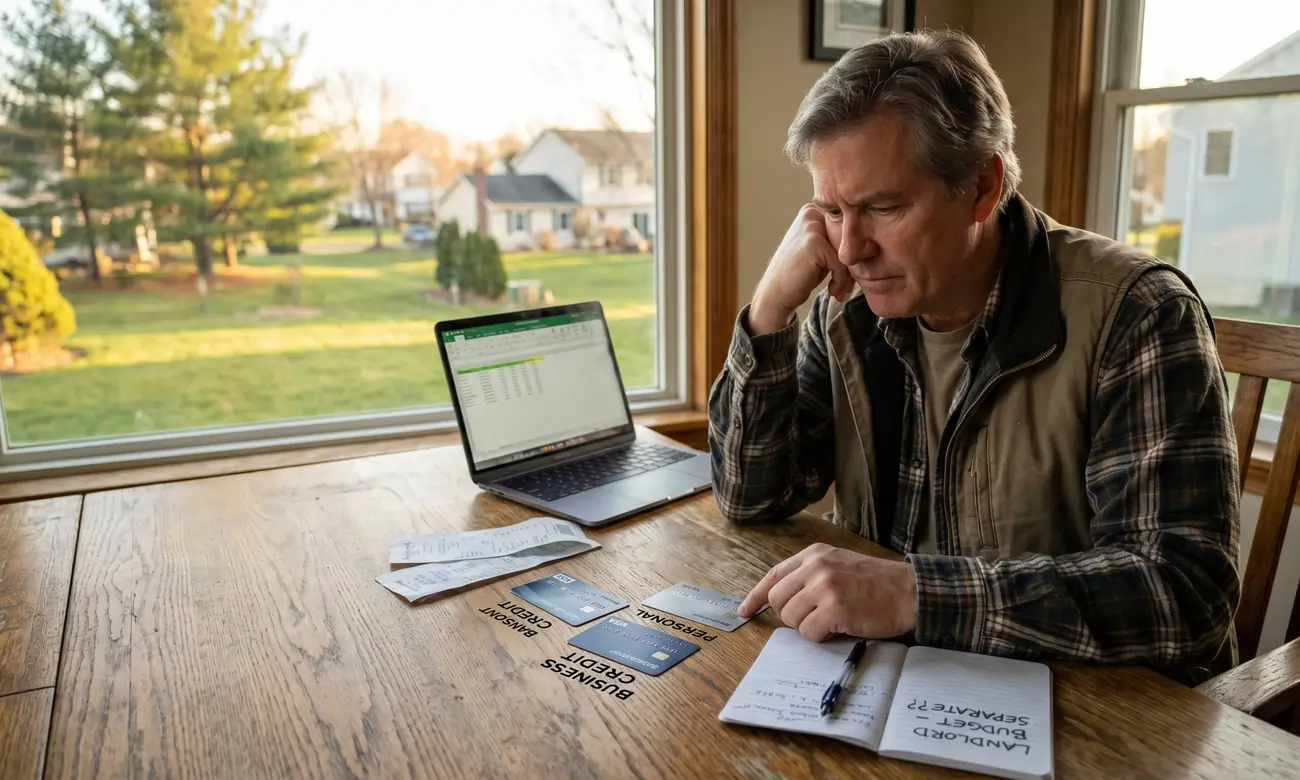

But even with one property, mixing personal and rental finances quickly becomes frustrating - particularly when tax time comes around, and you are left trying to remember what was personal and what was related to the property (as well as finding the expenses amongst your personal information).

It makes bookkeeping harder, tax time more stressful, and it becomes almost impossible to see whether your rental properties are actually making money.

Separating your rental business finances from your personal finances is one of the simplest ways to get more organised and more profitable.

The problem with mixing business with pleasure

The problem with mixing personal and business finances under one account is:

- More time spent categorising transactions

- A higher chance of missing deductible expenses

- Greater risk of errors at tax time

- Less visibility into how your rental business is performing

It can also create problems if you are audited.

The IRS expects landlords to keep accurate records of rental income and expenses. When everything is mixed together, proving what was business-related becomes much more difficult.

Why Separating Your Finances Makes Life Easier

Creating a dedicated bank account and credit card for your rental business gives you a much clearer picture of your finances.

1. Easier Bookkeeping

When every rental-related transaction runs through one account, your records are automatically cleaner.

Instead of sorting through hundreds of personal transactions, you can immediately see:

- Rent collected

- Mortgage payments

- Repairs

- Insurance

- Property taxes

- Contractor invoices

That makes monthly bookkeeping faster and easier.

2. Simpler Tax Filing

Tax preparation becomes much easier when all of your rental expenses are already separated.

You are less likely to:

- Miss deductible expenses

- Double-count transactions

- Forget important records

Instead, you can quickly generate reports and hand them to your accountant or use them to complete Schedule E.

3. Know Whether Your Property Is Actually Making Money

Many DIY landlords know how much rent comes in each month, but not how much they actually make after expenses.

Once your rental finances are separated, you can clearly see:

- Which properties are profitable

- Where expenses are increasing

- Whether your cash flow is improving or declining

This makes it much easier to make better investment decisions.

4. Stronger Legal and Liability Protection

If you own properties through an LLC, keeping your business finances separate is especially important.

Using the same account for personal and business spending can weaken the legal separation between you and the company.

In some situations, this can make it easier for someone to argue that the LLC is not truly operating as a separate business entity.

5. Easier To Scale

The more properties you own, the harder it becomes to manage everything manually.

Separating your finances early makes it much easier to:

- Add more properties

- Work with a bookkeeper or accountant

- Apply for financing

- Track performance across your portfolio

- Use digital tools and software

How To Separate Your Rental Finances From Your Personal Finances

The good news is that you do not need an accountant, a complicated business structure, or multiple properties to do this.

Even if you only have one rental property, you can usually get set up in an afternoon.

Step 1: Open a Separate Account Just for the Property

The easiest first step is to open a separate checking account used only for your rental property.

You do not necessarily need a formal business bank account if you own the property personally. Many landlords simply open a second checking account and use it only for rent and property expenses.

From that point forward:

- Deposit all rent payments into this account

- Pay all rental-related expenses from this account

- Do not use it for personal purchases

If you own properties through an LLC, open the account in the LLC's name.

Step 2: Get a Separate Credit Card

Using a dedicated business credit card makes it easier to track repairs, supplies, travel, and other expenses.

It also gives you a separate statement each month, which simplifies bookkeeping.

Step 3: Move Existing Automatic Payments

Update any recurring transactions so they come from the new account.

This might include:

- Mortgage payments

- Insurance

- Utility bills

- HOA fees

- Property management fees

- Software subscriptions

Step 4: Create a Clear Owner Draw Process

If you need to take money from your rental business for personal use, do not simply pay personal expenses from the business account.

Instead, transfer money to your personal account and record it as an owner draw or distribution.

That keeps your business records clean.

Step 5: Use Dedicated Landlord Software

Once you have a separate account, connect it to rental property accounting software.

This allows you to automatically import and categorize transactions, making it easier to stay organised and generate reports.

Best DIY Landlord Bank Accounts

If you are just starting to get organised, you probably do not need anything complicated.

The best option is usually one that is easy to open, easy to use, and separate from your everyday spending.

Here are some of the most common choices landlords use in the US (please note that we are not sponsored or associated with any of these banks):

Good for landlords who want a traditional bank with local branches.

Pros:

- Large branch network

- Easy to open LLC accounts

- Integrates with most accounting software

Potential drawback:

- Monthly fees unless you maintain a minimum balance

Monzo can be a good option for DIY landlords who want a simple, modern app and do not necessarily need a formal business account.

Many landlords use a separate Monzo account just for rental income and expenses.

Pros:

- Very easy to set up

- Strong app experience and instant spending notifications

- Pots feature is useful for setting aside money for repairs or taxes

Potential drawback:

- Better for landlords with one or two properties than larger portfolios

- Business features are more limited than those of traditional business banks

Wise is particularly useful for landlords who live abroad, own US property from overseas, or move money internationally.

Pros:

- Easy to hold and transfer multiple currencies

- Lower international transfer fees

- Good option for overseas or expat landlords

Potential drawback:

- Less useful if all of your banking is domestic

- Not designed specifically for property management

Popular with small landlords and LLC owners.

Pros:

- No monthly fees

- High interest on balances

- Fully online

Potential drawback:

A common choice for landlords who prefer online banking.

Pros:

- No monthly fees

- Good app experience

- Easy integrations with bookkeeping tools

Potential drawback:

- Better for simple banking than complex cash management

Relay is popular with landlords and real estate investors because it allows you to create multiple sub-accounts.

For example, you can keep separate balances for:

- Security deposits

- Taxes

- Maintenance reserves

- Different properties

Pros:

- Multiple checking accounts under one login

- Good for portfolio landlords

- Easy expense organization

Potential drawback:

Mercury is often used by landlords operating through an LLC or larger business structure.

Pros:

- Strong for business banking

- No monthly fees

- Good for landlords with multiple entities

Potential drawback:

- Designed more for businesses than specifically for landlords

Should You Use a Personal Account or a Business Account?

If you own one rental property in your personal name, you may be able to use a separate personal checking account dedicated only to your rental business.

However, once you:

- Own multiple properties

- Operate through an LLC

- Have a partner

- Want better bookkeeping and reporting

A dedicated business checking account is usually the better option.

Common Mistakes To Avoid

When landlords first separate their finances, they often make a few common mistakes:

- Continuing to occasionally use the business account for personal spending

- Forgetting to move recurring bills to the new account

- Using cash without keeping records

- Mixing multiple properties and personal spending in one account again

The key is consistency. Once you create a dedicated account, use it only for your rental business.

Start Small, Get Organised

Separating your business and personal finances is one of the easiest ways to become more organised as a landlord.

It makes bookkeeping easier, tax filing simpler, and gives you a much clearer view of how your rental business is performing.

Even if you only own one or two properties today, setting up a separate account now will save you time and stress as your portfolio grows.

The sooner you separate your finances, the easier everything else becomes.

.jpg)