How to Report Rental Income on Your Tax Return: Complete 2026 Guide

The complete 2026 guide to reporting rental income on your tax return (Schedule E). Learn what counts as income, which expenses are deductible, and how to avoid an IRS audit.

Every landlord has had that moment - you're filling out Schedule E and suddenly wondering if that lease-breaking fee counts as income, or whether the portion of the deposit you kept for damages needs to be reported this year or last year. The IRS has specific rules about what counts as rental income, and getting it wrong means either overpaying or inviting an audit.

This guide breaks down exactly how to report rental income on your federal tax return, which expenses actually reduce your tax bill, and how to avoid the mistakes that trigger IRS scrutiny.

What Counts As Rental Income?

The IRS considers more than just monthly rent checks as taxable income. Here's what you actually need to report:

Standard Rent Payments

Monthly rent is taxable in the year you receive it, not the year it covers. The IRS uses "constructive receipt” - income is taxable when it becomes available to you, even if you haven't deposited the check yet. If a tenant Venmos you the January rent on December 30th, that's 2026 income, not 2027.

Advance Rent and Prepaid Amounts

Tenant prepays three months of rent? That's all taxable income the year you receive it, regardless of what months it covers. The same goes for lease-option payments or any other prepaid amounts that you're keeping. The timing of when cash hits your account determines the tax year, not the lease period it's meant to cover.

Lease Cancellation Fees

When a tenant pays to break their lease early, that's income. The IRS treats it like rent because it's compensating you for lost rental payments. Report it in the year you receive it.

Non-Cash Payments

If your tenant fixes your plumbing in exchange for reduced rent, the fair market value of that work is taxable income. Same for any goods or services received instead of cash. You need to report what that service would have cost if you'd paid someone else to do it.

Security Deposits

Here's where landlords get confused: security deposits aren't taxable when you collect them. They only become income if you keep part or all of the deposit - typically for damages or unpaid rent. If you return the full deposit, it never touches your tax return.

How To Report Rental Income On Your Tax Return

Most landlords report rental income on Schedule E (Form 1040). Here's how it works:

Schedule E: Your Rental Income Form

Schedule E Form 1040 lists each property separately with its income and expenses. The IRS wants consistency - rent payments, fees, and retained deposits go in the income section. Operating expenses get itemized below. Net income (or loss) from all your properties flows to your Form 1040.

This form also determines whether your rental activity is "passive", which matters if your expenses exceed income. Most rental real estate is automatically passive unless you're a real estate professional who materially participates in the business.

Timing: When You Get Paid Matters

Federal tax law cares about when money becomes available to you, not when a tenant's lease says rent is due. Late-year payments are a common trap - if your January 2027 tenant pays early on December 28, 2026, that's 2026 income. Mark it correctly or your returns won't match your bank statements.

Cash vs. Accrual Accounting

Most landlords use cash accounting: report income when you receive it, expenses when you pay them. It's simple and matches how your bank account actually works.

Accrual accounting (reporting income when earned, expenses when incurred) is allowed, but requires meticulous records and consistent application.

Unless you're running a large portfolio or have specific tax reasons to use accrual, stick with cash method. Note that Landlord Studio uses the cash accounting method as well

Electronic Filing and Documentation

Purpose-built rental property accounting and tax reporting software can help you navigate your Schedule E categories and flag issues. But the software is only as good as your records. You still need organized receipts, invoices, lease agreements, and bank statements to back up what you're claiming - especially if you get audited.

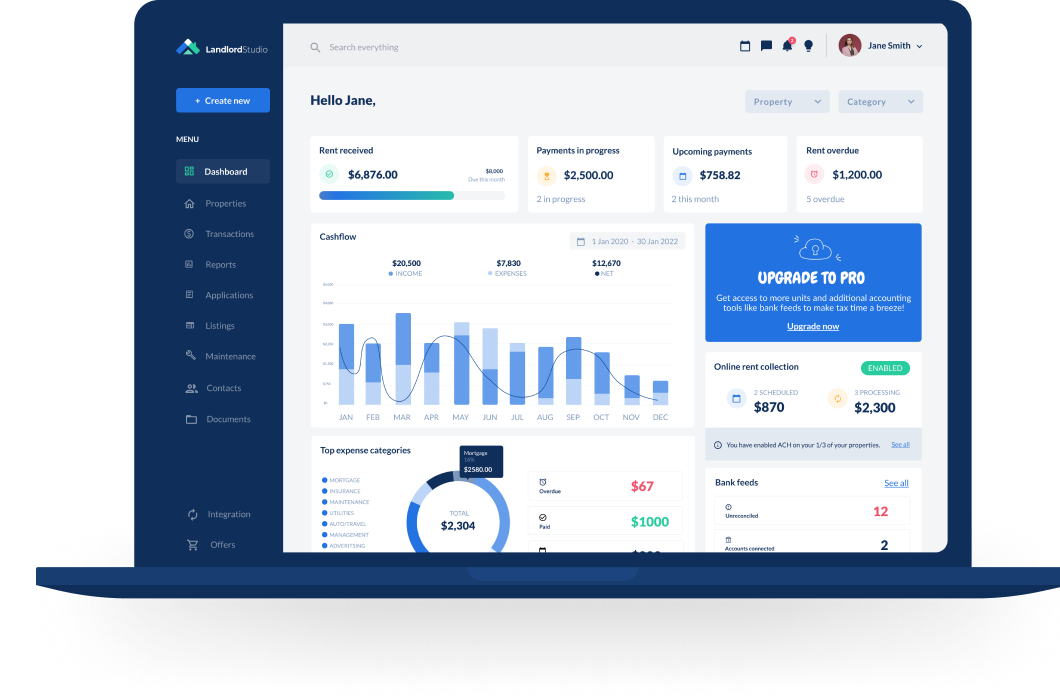

This is where property management software saves you. Landlord Studio automatically logs and categorizes rental income as it comes in, tracks which deposits you've returned versus kept, and generates the reports you need for Schedule E. No more hunting through bank statements in March trying to remember if that $1,200 charge was February rent or a deposit you returned.

Create your free Landlord Studio account today to streamline your rental property accounting and maximise your end of year deductions.

Deductible Expenses That Reduce Your Taxable Income

Once you've reported all income, deductions determine what you actually owe. Here's what the IRS lets you write off:

Operating Expenses

Routine costs tied to running your property are fully deductible the year you pay them:

Repairs and maintenance

Property management fees

Insurance premiums

Utilities you pay

Advertising for tenants

Cleaning and pest control

HOA fees

These are the everyday costs of being a landlord. As long as they're ordinary and necessary for your rental business, they reduce your taxable income dollar-for-dollar.

Depreciation

Residential rental buildings depreciate over 27.5 years. This is often your largest deduction, especially on newer properties. You depreciate the structure, not the land - so you need to separate the building value from the land value when you calculate this.

Major improvements - new roof, HVAC system, kitchen remodel - get depreciated separately based on their recovery periods. This is complex enough that most landlords run it past an accountant the first time.

Mortgage Interest and Property Taxes

Interest on loans used to buy or improve your rental property? Fully deductible. Property taxes on that rental? Also fully deductible. Your mortgage lender's year-end statement shows the interest amount. Your county sends a property tax bill. Both go on Schedule E.

Note: This only applies to the rental property. Your personal residence is a separate tax situation.

Repairs vs. Improvements: The Expensive Distinction

The IRS draws a hard line here:

Repairs restore property to working condition (fixing a leaky pipe, patching drywall, replacing a broken appliance). Deduct the full cost this year.

Improvements add value or extend the property's life (new roof, kitchen renovation, adding a deck). You have to depreciate these over multiple years.

Get this wrong, and you're either missing deductions or catching attention from an auditor. When in doubt, ask your accountant - or use software that prompts you to categorize each expense correctly as you enter it.

Driving to your rental for inspections, repairs, or tenant meetings? Track that mileage - it's deductible. Same for actual costs if you're flying somewhere for property management.

Administrative expenses also count: property management software subscriptions, office supplies, legal fees, accounting costs. If you're spending money to manage your rental business, it's likely deductible.

These errors either cost you money in missed deductions or invite audits:

Omitting Income

Forgetting to report that lease-breaking fee, or the last month's rent a tenant prepaid, or the $800 you kept from a security deposit - these omissions show up when the IRS compares your Schedule E to your bank records. Even small amounts matter.

Misclassifying Personal Expenses

You can't deduct repairs to your own home as rental expenses. You can't deduct your commute to work. You can't claim your personal cell phone bill just because you occasionally text tenants. The IRS sees this constantly and it's a red flag for audits.

Treating Improvements as Repairs

Replacing a broken water heater with the same model? Repair - fully deductible this year. Upgrading to a tankless system while you're at it? Improvement - depreciate over time. Claiming a $15,000 kitchen renovation as a repair will absolutely catch an auditor's attention.

Depreciation Errors

Depreciating land (you can't), using the wrong recovery period, or failing to separate the building value from land value - these are common errors that either inflate your deductions illegally or leave money on the table.

Inconsistent Accounting Methods

If you report 2025 income on a cash basis and then switch to accrual in 2026, you'll create discrepancies that confuse auditors. Pick a method and stick with it. If you need to change, there are IRS procedures for that.

Ignoring State Tax Rules

Federal rules are one thing. Your state might treat rental income differently, have different deduction limits, or require separate forms. Don't assume your state follows federal guidelines - check your state's tax agency or ask your accountant.

The goal isn't perfect tax knowledge. It's having a system that makes accuracy easier than guessing.

Track Everything as It Happens

Don't wait until tax season to categorize nine months of transactions. Record rent payments when they arrive. Log expenses when you pay them. Photograph receipts before they fade.

Software like Landlord Studio automatically categorizes income and expenses, tracks which deposits you've kept versus returned, separates repairs from improvements, and generates Schedule E reports. It syncs with your bank so you're not manually entering transactions.

This isn't about being lazy - it's about eliminating the human error that causes tax problems. When software categorizes a new roof as a capital improvement instead of a repair, you're not accidentally claiming a deduction you shouldn't.

Separate Personal and Rental Finances

Open a dedicated bank account for your rental properties. All rental income goes in. All rental expenses come out. Your Schedule E should match this account's activity almost perfectly.

Mixing personal and rental finances is how you accidentally deduct personal expenses or forget rental income. Separate accounts = clearer records = easier audits (if that ever happens).

Stay Current with IRS Rules

The IRS updates guidance on depreciation schedules, expense deductibility, and income recognition periodically. Publication 527 (Residential Rental Property) is your reference guide. Skim it annually or when you're making a big property decision.

Work With a Tax Professional

If you own multiple properties, have complex leases, or received significant non-cash payments, hire a CPA who works with landlords. Even a one-time review can catch expensive mistakes and optimize your deductions.

Most landlords can handle their own taxes with good software. But if your situation is complicated, professional advice costs less than an audit.

Bottom Line: How To Report Rental Income

Reporting rental income correctly isn't complicated - but it is specific. The IRS wants every dollar of income reported: rent, fees, deposits you keep, non-cash payments, all of it. Then you deduct legitimate expenses: operating costs, depreciation, mortgage interest, repairs, and more.

The difference between overpaying on taxes and getting audited is usually just organization. When you track income and expenses as they happen - ideally with software that makes categorizing everything easy - Schedule E becomes a 30-minute annual task instead of a weekend-long panic.

Because the point of owning rental property isn't to become a tax expert. It's to generate cash flow. And accurate tax reporting protects that cash flow by maximizing your deductions while keeping the IRS off your back.

Get ahead of your rental income and expenses and instantly generate tax-ready reports with Landlord Studio. Maximize revenue and make tax season a breeze with rental property accounting tools designed for you.

Monthly rent, advance rent, lease-breaking fees, security deposits you keep, and the fair market value of goods or services received instead of cash. Basically, if it compensates you for providing housing, it's taxable income.

Which form do I use to report rental income?

Schedule E (Supplemental Income and Loss), which attaches to your Form 1040. It lists each property's income and expenses separately.

Are security deposits taxable?

Not when you collect them. They become taxable only if you keep part or all of the deposit - usually for damages or unpaid rent. If you return the full amount, it never hits your tax return.

Can I deduct mortgage interest on my rental property?

Yes. Interest on loans used to buy or improve a rental property is fully deductible, as are property taxes tied to that rental. Your lender's year-end statement shows the interest amount.

What's the difference between repairs and improvements for taxes?

Repairs restore property to working condition and are fully deductible the year you pay them. Improvements add value or extend the property's useful life and must be depreciated over multiple years. This distinction matters - mess it up and you'll either miss deductions or trigger an audit.

Should I use cash or accrual accounting?

Most landlords use cash accounting: report income when received, expenses when paid. It's simpler and matches how your bank account actually works. Accrual accounting is allowed but requires consistent application and detailed records. Stick with cash unless your accountant recommends otherwise.

About Landlord Studio

Landlord Studio is an easy to use property management and accounting software designed for landlords.

Find and screen tenants, collect rent online, track income and expenses, run reports, and more - all for free.

Get weekly tips, tax updates, and landlord strategies straight to your inbox.

Thanks for subscribing. Check your inbox, your first update is on the way.

Oops! Something went wrong while submitting the form.

Managing Tenant Turnover and New Leases

Help fill your vacancies faster, choose better tenants, and start the next lease on the right foot - without creating compliance or cash flow problems.

Details:

Free

Hosted by:

Matt Hardy

When:

June 24, 2026

(1:00pm PT / 4:00pm ET)

Duration:

45 minutes + Q&A

Guest:

Lucas Hall, 15+ years in PropTech, Experienced Landlord and Real Estate Investor

.jpg)

.jpg)

.jpg)