Home Buying and Selling Property Reforms 2026 (Guide)

The UK's 2026 home buying reforms promise sales packs, binding contracts and a digital-first process. Here's what they mean for landlords and investors.

Industry News

Written by

Ryan Green

PUBLISHED ON

June 23, 2026

UPDATED ON

July 2, 2026

READ TIME

0 min

Read summarised version with:

ChatGPT

Gemini

Claude

Grok

Add as preferred on Google

On 19 June 2026, the government unveiled what's being called the biggest shake-up of home buying and selling in a generation - reforms designed to speed up moves, cut wasted costs and stop so many deals collapsing. For most people that's welcome news, because buying or selling a home in England and Wales has long been one of the slowest, most stressful financial transactions you can take on.

If you're a landlord or investor, it's worth more than a passing glance. You move through this system more often than most, and the things being reformed - fall-throughs, sluggish conveyancing and slow waiting times are the exact frictions that eat into your time and money on every acquisition and sale.

Here's what's actually being proposed, what it could save you, and when any of it might realistically land.

What has the government actually announced?

The reforms were published as a roadmap following a consultation, setting out how the government wants to transform the process over the course of this Parliament. The aim, in its own framing, is a system that is faster, clearer and cheaper for everyone involved.

There are five proposals worth knowing:

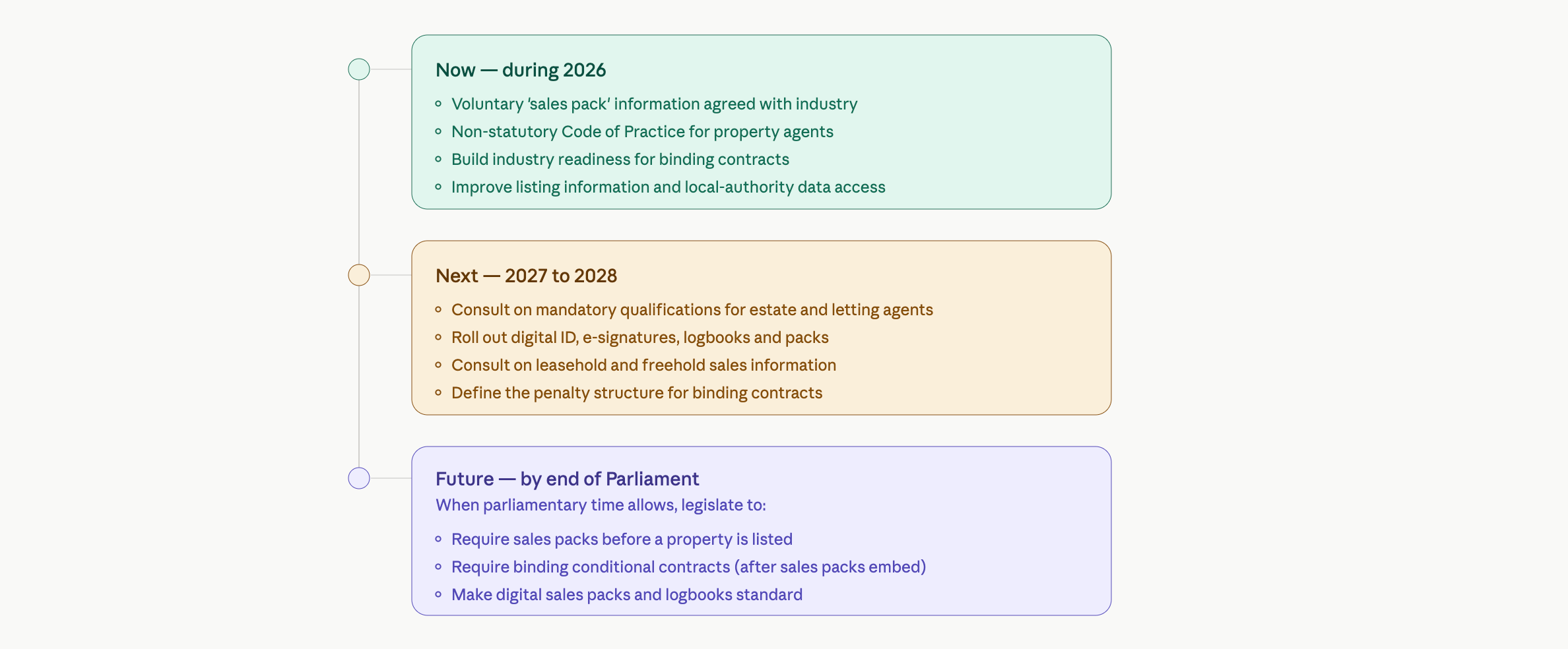

1. Upfront information - the 'sales pack'

Before a home goes on the market, the seller and their estate agent would have to put together a sales pack: the property's condition, title, leasehold costs and service charges, and where it sits in the chain. This means that buyers know up-front what the deal-breakers are before money and time is spent investigating it.

Under the current system, most of the real due diligence happens after an offer is accepted. The buyer pay for searches, a survey and the early legal work over several weeks and hundreds of pounds down. If that kills the deal, the money is simply gone.

2. Earlier binding (conditional) contracts

Today in England, either side can walk away at almost any point before exchange, often with no real consequence.

The proposal introduces binding conditional contracts that commit both parties much earlier with a financial penalty for pulling out without a valid reason.

"Conditional" is the important word. The commitment comes with legitimate get-outs: you'd still have a window to confirm finance, review the survey and check the title. If something genuinely doesn't stack up, you have a route out. If it's all fine, the deal proceeds with far less risk of collapse.

For investors running frequent transactions, fewer late collapses is the headline benefit here.

3. A digital-first process

At the heart of the package is a shift away from paper. The government wants digital property logbooks, digital identity checks, electronic signatures and even AI-assisted conveyancing, so the same information isn't re-keyed and re-verified by every party in the chain.

If this feels familiar, it should. It's the same direction of travel as Making Tax Digital for landlords - records kept digitally once, then reused, rather than rebuilt from scratch each time. Tools like electronic signatures are already standard practice for forward-thinking landlords.

4. Tighter rules for estate agents

Estate agency in England is effectively unregulated. There's no licence or mandatory qualification to start selling people's homes.

The government proposes a new Code of Practice, with mandatory qualifications to follow. For anyone who has had a frustrating agent experience, a higher baseline standard is hard to argue with.

5. Clearing the bottlenecks

The final strand tackles the of efficiency: reducing duplicated anti-money-laundering checks, addressing how long (and how much) freeholders and managing agents can take to hand over leasehold information, and continuing to digitise HM Land Registry and local-authority data that everything else waits on.

Why so broken? Three things compound: the information you need arrives late, nobody is truly committed until the very end, and far too much still runs on paper and duplicated checks.

How other countries do it better

The UK doesn't have to work this way - and the government has pointed to systems that already work better. The Netherlands, Norway and Finland are all cited as examples where digitised, transparent processes deliver faster, more certain moves.

For landlords, the bigger prize is in the deals that don't collapse. A late fall-through can cost you a survey, searches and a chunk of legal fees - easily one to three thousand pounds for nothing. If you're transacting regularly, cutting that risk is real money back in your pocket, plus far less wasted time.

The whole reform also leans on going digital - logbooks, e-signatures, records shared once and reused. That's exactly the shift already underway for landlord finances under Making Tax Digital. The landlords who'll find the next few years easiest are the ones who've already moved their record-keeping off spreadsheets and paper.

Worth noting: if you're selling a tenanted property, the rules that affect you most right now aren't these conveyancing reforms but the Renters' Rights Act - see our guide to selling under Ground 1A.)

When will the changes actually happen?

The two changes that matter most- mandatory sales packs and binding contracts both need new legislation, and the government's timeline runs across this Parliament rather than this year. A new Code of Practice for estate agents is expected sooner, with consultation on agent qualifications following in 2027.

So it's a real plan, just a gradual one. Don't expect your next purchase to feel dramatically different. The direction is genuinely right; the timeline is the usual Westminster "as soon as practicable".

The bigger picture for landlords

The reforms should, over time, make buying and selling smoother - and for active investors, fewer collapsed deals is a meaningful win. But a faster checkout doesn't change the economics of a deal. Whether a property actually works as an investment is decided by the numbers: the yield, the costs, and what you keep after tax.

That's the part you control today. Landlord Studio is HMRC-recognised Making Tax Digital software built for UK landlords. You can track income and expenses across your portfolio, capture every allowable expense, and keep digital records that are ready for HMRC and your accountant. When the market does speed up, you'll already know exactly which deals are worth doing.

About Landlord Studio

Landlord Studio is an easy to use MTD compliant property management and accounting software designed for UK landlords. Track income and expenses, run reports,, find and prescreen tenants, manage property maintenance, and more.

Get weekly tips, tax updates, and landlord strategies straight to your inbox.

Thanks for subscribing. Check your inbox, your first update is on the way.

Oops! Something went wrong while submitting the form.

Costly MTD Mistakes & How to Fix Them

94% of landlords feel ready for MTD. Only a third have moved to digital software. Join our live panel on the costliest MTD mistakes and how to fix them.

Details:

Free

Hosted by:

Logan Ransley

Kate Faulkner

Martin Wardle

When:

August 11, 2026

12PM

Duration:

45 mins + Q&A

Format:

Live Panel Discussion

Guest:

Co-host Logan Ransley, Landlord Studio Co-Founder

Kate Faulkner OBE, the UK's Leading Property Expert

.webp)

.webp)